Picking a student loan that meets your needs requires an understanding of some basic concepts. Student Loan Basics empowers you with information to make informed choices to borrow for college. This article explains loan amortization and shows how to pay off student loans faster.

Definitions

Don’t let the fancy word amortization intimidate you. Amortization is simply the process of paying off your loan.

Each loan payment has two parts:

- Interest

- Principal

The amortization schedule for a loan shows how each monthly payment is split between paying interest and principal due.

Principal is the amount you initially borrow. Interest is the fee charged for borrowing the money.

The loan term is the number of years you have to fully repay a loan. Most student loans initially have a standard loan term of 10 years.

For a 10-year loan, the amortization schedule will show 120 payments with the dollar amount of the principal that will be paid off that month and the interest charge.

To make it easier to budget loan payments in the future, student loans require a fixed payment amount each month. From the first payment to the second to last payment, you will be required to pay the same amount each month.

The very last payment is usually less than the other payments. Why? The total of the remaining outstanding principal and the interest owed is less than the fixed monthly payment. It feels great to send that last chunk of change to pay-off the loan.

Sample Amortization Schedule: Minimum Monthly Payment

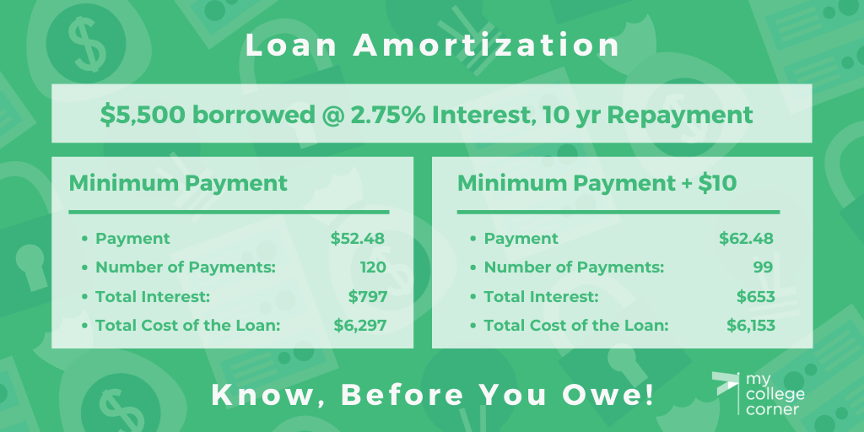

To keep this from getting too complicated too fast, let’s look at an amortization table for a federal Direct loan for which a college freshman would be eligible:

- Principal: $5,500

- Loan Term: 10 years

- Interest Rate: 2.75%

The minimum monthly payment to amortize this loan is $52.48/month. The chart below shows the part of the payment that is applied to principal (blue) and the amount applied to interest (green). In the 12th month, $40.89 of the payment is applied to principal. The final payment (month 120) includes $52.34 of principal.

Notice a few things:

- The amount of principal being repaid in each period is increasing

- The amount of interest being paid each month is decreasing

- The total amount of interest paid = $797

How to pay-off your loan faster

There is no magic bullet to make your principal balance go down quickly – you have to make larger payments. The magic occurs in realizing that relatively small increases in the monthly payment could significantly reduce the time it takes to repay to loan. Shortening the repayment period reduces the amount of interest paid and the total cost of the loan.

Sample Amortization Schedule: Minimum Monthly Payment plus $10/month

See what happens if an extra $10 per month is added to the minimum monthly payment. The $5,500 loan is now amortized with a payment of $62.48.

Any extra amount of payment above the required minimum monthly payment will reduce the principal outstanding dollar for dollar by the amount of the overpayment. By increasing the monthly payment by an amount equal to several cups of coffee each month, the loan is paid off almost two years earlier with a total savings of nearly $150.

You might be thinking that saving “only” $150 in total interest is not much. The primary reason the total interest savings is so low in this example: interest rates have been at record lows. If the interest rate were greater, the dollar amount of savings would also be greater. In any case, would you rather have $150 in your pocket or send it to a bank?

Summary

Understanding the basic concept of loan amortization could help you pay down your student loan faster.

In our example above, a borrower who added $10/month was able to dramatically cut-down the time it took to pay-off the loan and saved some money as well.

It’s vital to understand the basics of student loans before you select one. As we like to say: know before you owe.

More Information

For more information about student loans, the blog at MyCollegeCorner.com posted these Student Loan Basics articles: